W-2 Employee vs. 1099 Independent Contractor: Understanding the Key Differences

W-2 Employee vs. 1099 Independent Contractor: Understanding the Key Differences

As careers become more flexible and non-traditional, many professionals find themselves choosing between working as a W-2 employee or a 1099 independent contractor. Each structure comes with distinct advantages, trade-offs, and planning considerations.There is no universally “better” option. The right choice depends on income stability, benefits, lifestyle preferences, risk tolerance, and long-term goals. Understanding the differences can help you make more informed decisions about your career—and your financial life.

What Is a W-2 Employee?

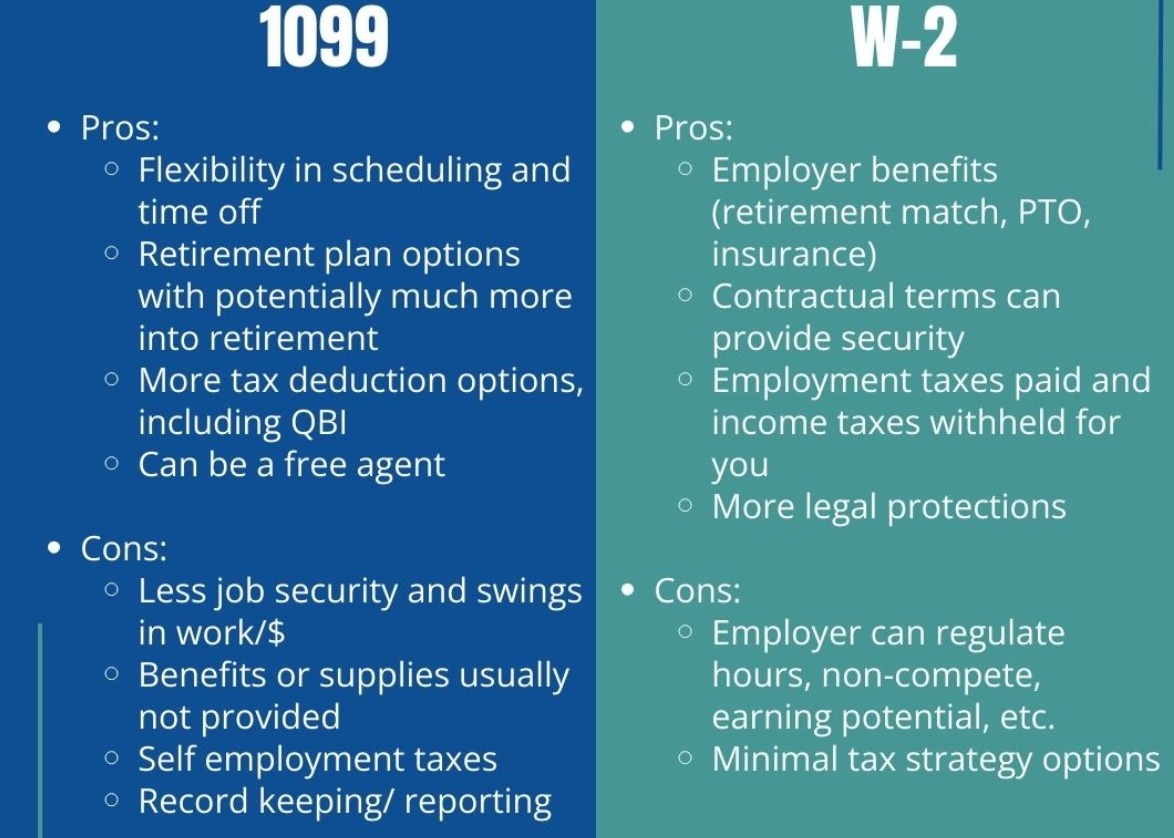

A W-2 employee works directly for an employer. The employer controls how, when, and where the work is performed and is responsible for withholding payroll taxes and providing certain benefits.

Advantages of W-2 Employment

Income Stability

Many employees value the predictability of a regular paycheck. This can make budgeting and cash-flow planning more straightforward.

Employer-Provided Benefits

W-2 roles often include benefits such as:

- Health insurance

- Retirement plans (e.g., 401(k) with potential employer contributions)

- Paid time off and holidays

- Disability or life insurance

Simpler TaxesPayroll taxes are automatically withheld, and tax filing is generally more straightforward.

Reduced Administrative BurdenEmployees don’t need to manage invoicing, contracts, or business expenses.

Disadvantages of W-2 Employment

Less Flexibility

Work schedules, locations, and responsibilities are typically defined by the employer.

Limited Tax Planning Opportunities

Employees have fewer deductions available compared to business owners or contractors.

Income Ceiling

Raises and bonuses are usually constrained by company policy, budgets, or compensation bands.

What Is a 1099 Independent Contractor?

A 1099 contractor is considered self-employed and provides services to clients or companies under contract. Contractors control how the work is performed and are responsible for managing their own taxes and benefits.

Advantages of 1099 Work

Greater Flexibility and Autonomy

Contractors often have more control over:

- Work hours

- Client selection

- Work location

- Scope of services

Potential for Higher Income

Because contractors take on more responsibility, compensation may be higher—especially for specialized skills.

Expanded Tax Planning Opportunities

Self-employed individuals may deduct ordinary and necessary business expenses and have access to retirement plans designed for business owners.

Career Optionality

Many professionals appreciate the ability to diversify income across multiple clients rather than relying on a single employer.

Disadvantages of 1099 Work

Income VariabilityPay can fluctuate based on workload, client demand, or economic conditions.

Self-Funded Benefits

Contractors must arrange and pay for their own:

- Health insurance

- Retirement savings

- Paid time off

- Insurance coverage

Tax Complexity

Contractors are responsible for:

- Quarterly estimated taxes

- Self-employment taxes

- Record-keeping and compliance

Higher Personal Risk

There is no built-in job security, and legal or financial protections may be more limited.

Key Planning Considerations

When evaluating W-2 versus 1099 work, it’s helpful to look beyond headline income and consider:

- After-tax take-home pay

- Cost of benefits and insurance

- Lifestyle flexibility

- Career longevity and growth

- Risk tolerance

- Administrative responsibilities

Many professionals also transition between these structures over time—or combine both—depending on their stage of life and career priorities.

The Bottom Line

W-2 employment and 1099 contracting each serve different needs. One offers structure and predictability; the other offers flexibility and control. Neither is inherently better—it’s about alignment with your personal and financial goals.

Thoughtful planning can help ensure that whichever path you choose supports not just your income, but your overall quality of life.

Career decisions don’t exist in isolation—they affect taxes, benefits, cash flow, and long-term planning. Having clarity around how your work structure fits into your broader financial picture can make a meaningful difference.